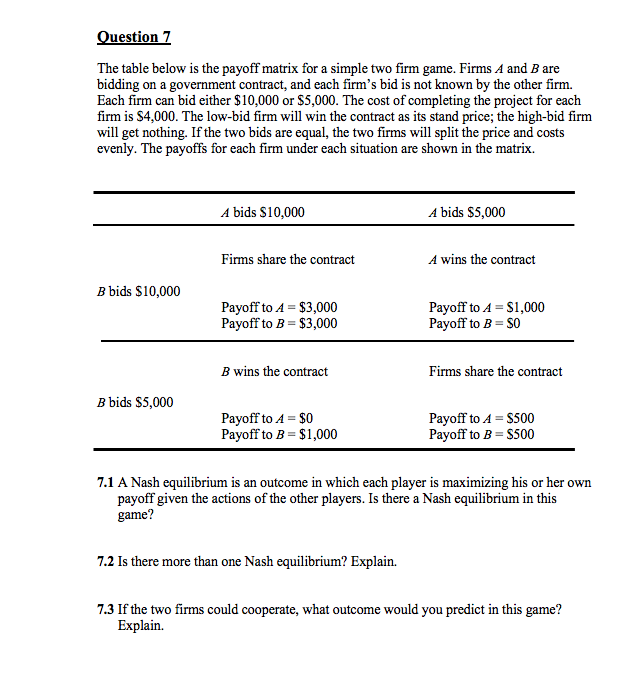

FHA financing are only among the many financial situations your are able to use when buying a house. They are secured of the Government Houses Government — a beneficial U.S. company were only available in 1934 while making homeownership economical — and will be taken on unmarried-household members property, also one or two-product-, three-device, and you may five-device characteristics (as long as you live in one of the devices).

Because of the government’s ensure — meaning the latest FHA commonly reimburse the lending company in the event the a borrower non-payments on the mortgage — these mortgage loans include reduced costs and you can lowest credit rating minimums and require simply a decreased down-payment.

FHA money commonly for everybody, no matter if, there is rigid limits about how precisely far you can use with the mortgage loans. When you’re wanting using an enthusiastic FHA financing in your second purchase, here is what you must know concerning FHA loan limitations close by.

Just how are FHA loan limits determined?

FHA mortgage limits are derived from the fresh new conforming financing maximum lay by Federal Housing Fund Agencies as well as the average domestic price in every provided urban area. Inside reduced-costs areas, this new FHA loan limitation was 65% of your own compliant mortgage limit regarding county. Within the highest-costs of these, it is 150%.

Financing restrictions along with are very different by the possessions dimensions. One-unit features, such as for instance, has a smaller sized loan restriction than just a couple-, three-, otherwise four-unit qualities. So that the highest possible FHA loan limitation? You will notice one for the four-device features from inside the large-costs locations.

Exactly what are the FHA financing restrictions within the 2022?

As the home prices are always for the flux, FHA mortgage restrictions — plus FHFA compliant mortgage limitations — try modified per year. In both cases, this new constraints improved inside the 2022.

This present year, brand new baseline FHA restrict with the solitary-friends features was $420,680 for many of the country. Maximum from inside the higher-prices segments try $970,800, a bounce regarding $822,375 the season previous.

Special credit restrictions can be found having borrowers during the Alaska, Their state, Guam, additionally the Virgin Isles because of high framework costs in these areas. This is how men and women restrictions fall apart:

- One-device functions: $step 1,456,2 hundred

- Two-tool attributes: $1,864,575

- Three-unit features: $dos,253,700

- Four-equipment qualities: $dos,800,900

If you want to understand the direct FHA loan restrictions getting a place you’re thinking about to acquire within the, your best bet is the FHA’s browse equipment. Simply input a state, state, and you will restriction sorts of, and you may comprehend the mortgage restrictions regarding city inside mere seconds.

You will possibly not qualify for the utmost loan amount

The FHA mortgage constraints are only that the main picture. Quite simply, even though the latest FHA was happy to ensure good $step 1.5 million-dollars home loan in your area doesn’t invariably mean that your is also qualify in order to borrow that much.

Loan providers believe a number of different aspects whenever choosing simply how much your normally obtain, in financial trouble-to-money proportion, or DTI, being chief included in this. It’s online tribal personal loans your month-to-month debt burden separated by the pre-tax month-to-month money, conveyed given that a percentage. For example, when your payment per month financial obligation was $2,000 a month and you also earn $5,000, your own DTI is 40%.

- Your revenue.

- The pace in your FHA loan.

- Your expected possessions fees, insurance, and people association (HOA) charge on your new home.

- Their lender’s limit DTI proportion (which are lower than maximum allowed by FHA).

- The fresh new FHA mortgage limitation close by.

Understand that there are 2 types of DTI percentages. The front-prevent DTI is the portion of your earnings that will go toward your homeloan payment. The rear-stop DTI ‘s the percentage of your earnings that will go on all of your monthly obligations, together with your mortgage payment.

Even though many lenders provides front side-prevent DTI maximums getting FHA funds, the trunk-stop DTI ratio ‘s the more significant of these two when you are looking at loan approval, very expect a loan provider to adopt your own other financial obligation fee financial obligation directly.

The high quality FHA straight back-prevent DTI limit is actually 43%, nonetheless it may go high when you have precisely what the institution phone calls “compensating circumstances.” This might tend to be an extremely higher downpayment, a clean bank account, or a very good credit rating.

Greatest Mortgage lender

It is vital to think multiple mortgage brokers to obtain an effective complement you. We now have noted a favourite lenders lower than so you can examine the options:

All of our ratings are derived from a top measure. 5 famous people equals Top. cuatro a-listers translates to Advanced. step three famous people equals A. dos superstars translates to Reasonable. step one star translates to Bad. We need your money to function more difficult to you. That’s the reason all of our studies are biased on the now offers you to deliver liberty when you find yourself eliminating-of-pouch will set you back. = Better = Higher level = An excellent = Fair = Terrible

Most other FHA conditions

Except that the DTI, there are many more conditions you’ll need to fulfill in order to qualify for an enthusiastic FHA home mortgage. Let me reveal a look at the agency’s most recent mortgage criteria:

FHA fund additionally require a home loan Premium, which you can shell out on closing and along side life of the financing. Up front, the purchase price was 1.75% of your amount borrowed. A year, the MIP will set you back is dependent upon your loan matter and down payment.

The conclusion

FHA financing restrictions change annually, and if you are interested in by using these reduced-rates loans for your upcoming funding, ensure that you may be up to date for the current wide variety. For additional information on FHA funds, find our FHA loan publication and try all of our greatest FHA lenders.